TLA continuously researches and monitors economic and market trends on behalf of the families we serve.

Leaving on a Jet Plane 🎵 (or not)

Two unrelated air travel narratives. First, I am planning to visit my son and his family this summer. I casually looked at the flights a few weeks ago and then again this past weekend when we confirmed the best dates to visit. In those 3 weeks, the price went up an astounding 70%. My guess is that unless the prices come down fairly soon, staycations may be very popular this summer. When added to the reduced visitation from overseas, this could be a weaker-than-expected season for the travel industry.

Second, Delta Airlines announced it is suspending VIP services, airport escorts, and “Red Coat” assistance for members of Congress due to their inability to properly pay TSA workers. Imagine public servants being treated as regular passengers.

The Company Store 🎵

Jerome Powell has likely chaired his last Federal Reserve Open Market Committee meeting. Referring to the tariff confusion, lackluster job market, and still sticky inflation, Chairman Powell concluded that “There is no free lunch.”

We have entered a period of maximum Fed uncertainty with risks skewed to the upside for both inflation and unemployment. Just as the tariff-induced tension in the Fed’s dual mandate (stable prices and full employment) was beginning to fade, the current risk assessment shows they may be right back where they found themselves in 2022 when the Fed felt forced to raise rates just to catch up to inflation realities.

Higher energy prices today certainly complicate the Fed’s decision-making. Fed expectations have quickly moved from 2 likely cuts in 2026 to only a 30% chance of any cuts in 2026. In fact, if we see the Fed cutting anytime soon, it’s most likely for bad reasons, such as slowing growth and/or labor market deterioration.

War – What’s it Good For? 🎵

Today, we have a totally new and mostly unanticipated concern to deal with – war in the Middle East.

While we may agree that a nuclear-free Iran is a very good thing, no one knows how long this conflict will last, and at what cost, in both human and economic terms. Countless dead and an estimated $1 billion per day that the U.S. Treasury must borrow. We all hope that peace will come soon, but as of this writing, the war in the Middle East continues as the US and Iran seem to be talking past each other.

In the meantime, no part of our economy is immune to energy price spikes. $90-$100+/barrell of oil will take a toll on the economy if it lasts much longer. Oil is one of those commodities that touches nearly every part of the economy, from the gasoline and diesel we put in our cars to the cost of groceries and manufactured goods. Oil prices that rise significantly can act as an extra “tax” on households and businesses. Rising energy costs can squeeze budgets and slow economic growth.

Unfortunately, producer prices were already in acceleration mode before the hostilities began, up 3.4% over the 12 months ending in February. Coffee, ground beef, household furnishings, home electricity, and computers were all up double-digit, and now air travel is skyrocketing. In a vicious cycle, inflation expectations beget further inflation. What matters is how long prices stay high, which will largely depend on geopolitical factors that are difficult to predict.

Sixteen Tons 🎵

At the same time, the labor market does not appear to be healthy. There’s been virtually no job growth since the end of 2024. Employers, perhaps unnerved by back-and-forth tariff policies, have largely been on strike for a year, resulting in more Americans looking for work than there are job postings.

The good news is that wages grew faster than inflation over the past year, which is a positive for both workers and consumer spending. This may help explain the continued strength in recent consumer spending, but a lackluster labor market threatens future consumer spending, which is the main driver of the U S. economy.

Money for Nothing 🎵

Let’s start with some economic positives: The effect of tariffs has been far more muted than many feared, and with full control of both houses of Congress, the president successfully navigated a huge tax and spending bill, designed to stimulate the economy this year. This includes $160 billion in tax refunds, up 14% from last year, potentially fueling consumer spending.

In addition, Corporate earnings remain strong, growing well above the long-term average. The Atlanta Fed’s Now-GDP model is forecasting a relatively healthy 2.0% GDP growth in the current quarter, and a recent ISM (Institute for Supply Management) survey showed surprising strength for both the manufacturing and services sectors.

The fact that the US stock markets remain near all-time highs may mean that investors, at least for now, are giving the president the benefit of the doubt, hoping for an economic resurgence.

At the same time, there’s no shortage of things to worry about. The U.S. economy seems to be riding a macroeconomic rollercoaster – oscillating between improvement and deterioration. Real GDP in the 4th quarter grew at an anemic 0.7%, the Conference Board’s Leading Economic Indicators (LEI) fell in January for the sixth consecutive month, and has fallen in 43 of the last 47 months.

The Wall Street Journal reported on March 18th that a record number of workers were raiding their 401(k)s. While there is no data yet on why, given that taxes plus penalties are due when 401(k)s are prematurely withdrawn, there is a high likelihood that loss of employment, unexpected healthcare expenses, and tapping out of credit cards are among the reasons.

Economic indicators point to continued strain on household finances. U.S. consumer sentiment fell in early March 2026 to a three-month low — reflecting concerns about rising gasoline prices tied to the war in the Middle East and the still-high cost of living.

The economic impact of a prolonged oil shock has been significant in the past (i.e. 1973-74 Yom Kippur war, 1979 Iran oil embargo, the 1990 Iraqi invasion of Kuwait, and 2022 Russian invasion of Ukraine), and the potential for a similar fallout should not be overlooked. The major difference today is that the U. S. economy is now less exposed to higher energy prices. For example, consumers now spend about 2% of disposable income on gasoline, down from roughly 6% forty years ago. On the demand side, we have increased fuel efficiency and battery-powered cars on the road. On the supply side, fracking has created a surge in oil and gas production. In fact, the U. S. is now a net exporter of 3 million barrels a day vs. a net importer of 9 million barrels just 15 years ago.

Our House 🎵

Last summer, we raised concerns about the housing sector. Updates are not encouraging. New home sales plunged in January, the biggest drop in 13 years. While poor weather conditions may be partially to blame, that does not explain why homebuilders remain broadly pessimistic today. Traditional mortgage rates briefly dipped below 6.00%, but have now risen for four straight weeks to about 6.40%. Higher mortgage rates plus rising insurance, property taxes, and utility bills create an affordability problem for current home-owners and potential home-owners.

Any housing slump would be extremely problematic for the US economy and consumer psychology. There are two reasons. First, 5% of the nation’s jobs are directly tied to the housing sector. Second is what may be referred to as the “wealth effect, ” which is the concept that consumers will spend more when rising asset prices make them feel richer, even if their disposable income hasn’t changed. If the value of their house increases, even if they are not making any more money, they are likely to spend more. Approximately 65% of homes are owner-occupied, meaning that over half of US consumers have wealth directly tied to housing.

Parenthetically, people are also more willing to spend more when they see the value of their 401(k) increase. The opposite is also true – when consumers see their wealth decrease, even if their income has not gone down, they tend to become more thrifty.

Golden Ring 🎵

The pawn shop business today can be a good indicator of how households are holding up because pawn activity tends to rise when household budgets are strained. Pawn shops across the country are seeing increased demand as financially strained consumers look for quick cash and lower-cost secondhand goods amid persistent pressure from inflation and economic uncertainty.

Industry experts say pawn shops have historically served as a real-time indicator of financial stress, particularly among consumers with limited savings or access to traditional credit. Typical pawn shop customers often lack access to traditional credit options, while others may already be carrying significant debt burdens.

American households owe $1.28 trillion in credit card debt, according to the latest data from the Federal Reserve Bank of New York. That’s a 5.5% jump from the year before.

A Tale of the Ticker 🎵

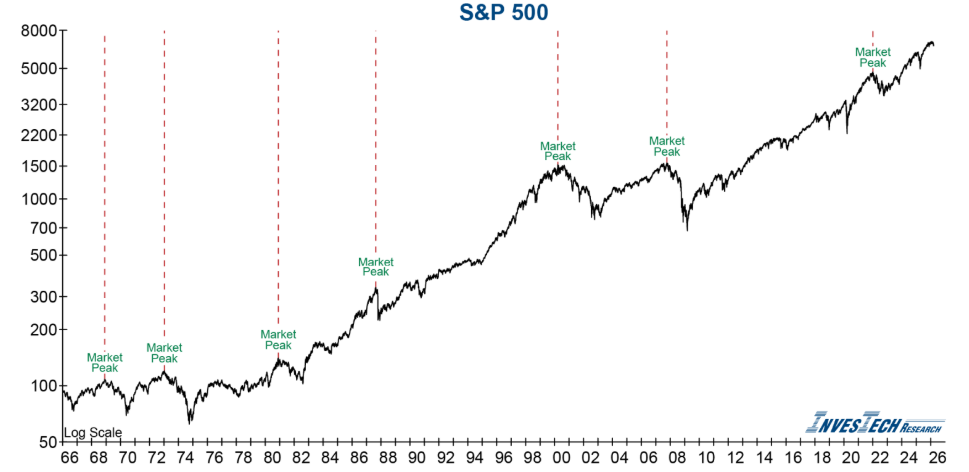

Just days ago, stocks were still within striking distance of all-time highs, and evidence indicates that while individual investors say they are worried, they, in fact, keep buying. As an example, a full 71% of 401(k) assets are allocated to equities. Loose financial conditions and a relatively strong economy since the Great Recession have encouraged some investors to stretch for out-sized returns. Some of the riskier bets from the last few years have paid off, giving more novice investors confidence that may not have been earned. While we don’t know when the next major market downturn will be, we likely know where it will be — at the epicenter of whatever has been most popular. Just think about what has been the most talked about, the most hyped on social media, and so-called business news shows over the last several years. That’s where the greatest danger most likely lurks.

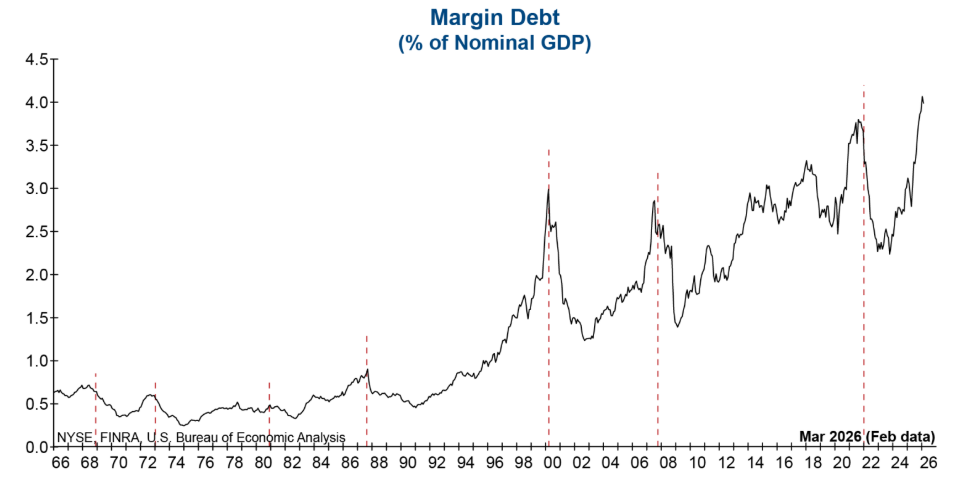

In the fall, we talked about margin debt as a useful tool for monitoring leverage and excesses in the stock market. Margin debt represents the amount of money borrowed by investors to buy more securities. We monitor margin debt as a percentage of GDP because downturns in this measure following a parabolic rise often precede or coincide with peaks in the market. Margin debt/nominal GDP recently hit an all-time high – far exceeding the peaks prior to the 2000 tech bubble and the great financial crisis.

Valuations still seem extreme. The CEO of Goldman Sachs recently said, “It’s likely there will be a 10-20% drawdown in equity markets sometime in the next 12 to 24 months. As of this writing, the S&P 500 is down 6.5% year-to-date and down about 10% from its February high.

I Won’t Back Down 🎵

While we remain defensive, we don’t panic. Making dramatic portfolio changes in response to geopolitical events is, in fact, often counterproductive. The process of building a portfolio and wealth planning is designed to manage this uncertainty. While each event is unique, financial markets have navigated countless wars and regional conflicts. The key is for long-term investors to separate headlines from portfolio decisions.

Trying to anticipate and invest for a worst-case scenario has historically been an ineffective strategy, but proactively managing risk and adapting a portfolio as evidence unfolds has a solid track record in navigating uncertainty.

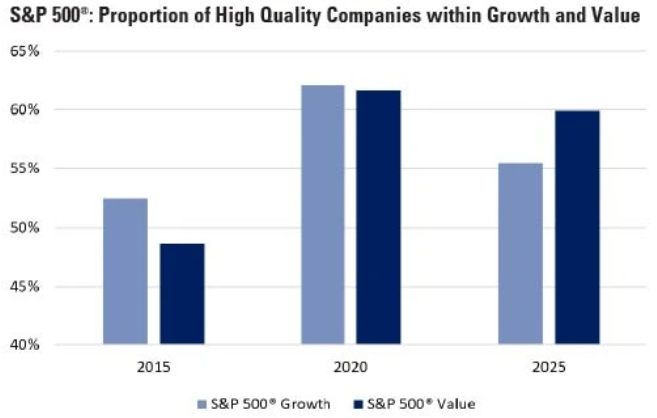

Case in point: For years, we saw evidence of more opportunity in so-called growth stocks than value stocks. We therefore overallocated to growth. Seeing the huge run-up in growth stocks, we reallocated portfolios in 2021 to a more even-weight allocation. Then in 2022, we mitigated some of the mini “tech-wreck” when we further reduced our allocation to growth in favor of value. We’ve maintained an important overallocation to value ever since. The chart below provides more confidence that, in this period of uncertainty, we are also allocated to higher quality companies – those with superior balance sheets and cash flows.

Source: Richard Bernstein Advisors LLC, S&P Global, Bloomberg Finance L.P.

While this is no time to become complacent, we will continue to follow the weight of the evidence and not overreact. We prefer a broadly diversified allocation in reasonably valued equities, bonds (including tax-free municipals for those in the highest tax brackets), and alternatives, all to create an asymmetrical portfolio that allows growth while “buffering” downside risk where possible.

– Andrew T. Gardener, CFP®